IRS 1041 2025-2026 free printable template

Get, Create, Make, and Sign IRS 1041

Instructions and Help about IRS 1041

How to edit IRS 1041

How to fill out IRS 1041

Latest updates to IRS 1041

All You Need to Know About IRS 1041

What is IRS 1041?

Who needs the form?

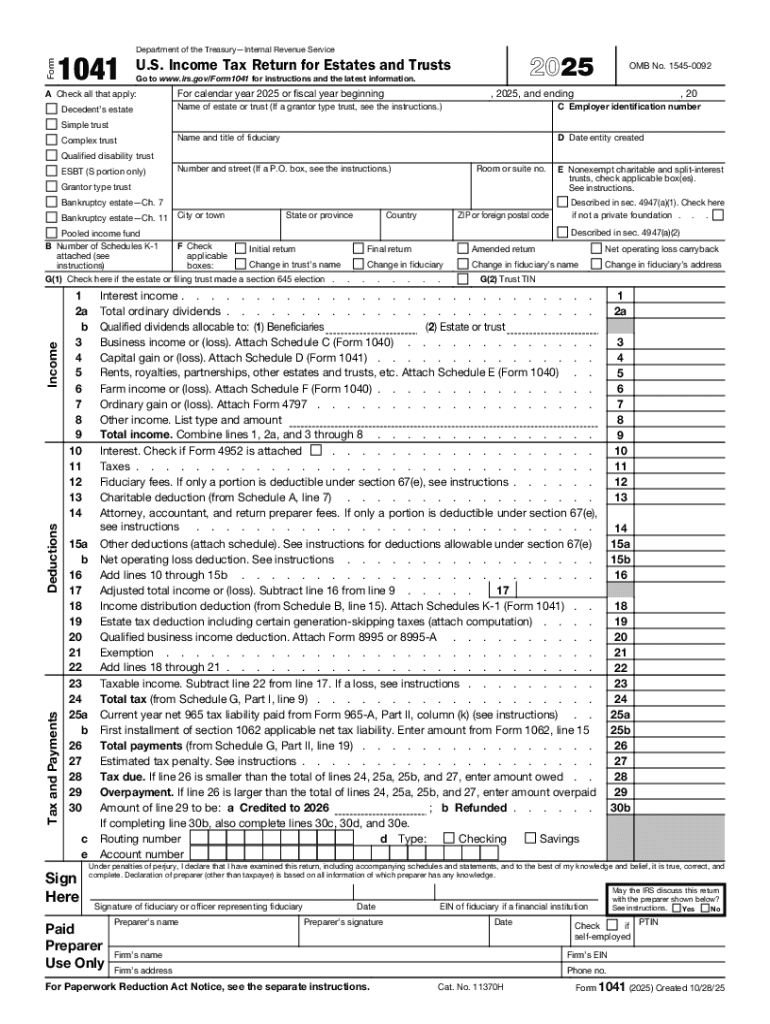

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 1041

What should I do if I made a mistake on my IRS 1041?

If you realize there are errors after filing the IRS 1041, you can submit an amended return using Form 1041-X. It's crucial to provide correct information and explain the reasons for the amendments to avoid potential penalties.

How can I track the status of my IRS 1041 after filing?

You can track the status of your IRS 1041 by visiting the IRS website or calling their helpline. When e-filing, ensure you have your confirmation number, as this will help in verifying the processing of your return.

What should I consider when filing the IRS 1041 as a nonresident?

Nonresidents may have additional considerations when filing the IRS 1041, such as specific tax treaties and reporting requirements. It’s advisable to consult a tax professional familiar with nonresident tax obligations to ensure compliance.

How long should I retain records after filing my IRS 1041?

Typically, you should retain your records related to the IRS 1041 for at least three years from the date of filing. This period is important in case of audits or if you need to reference past filings.